Ever find yourself crunching numbers with a calculator to see where you stand with your financial decisions? Well, that’s me! I’m that guy, always diving into the numbers to figure out the trade-offs in life. And lately, I've been thinking a lot about automobile insurance.

When my recent auto insurance bill arrived, I decided to dig into how these calculations actually work. Of course, everyone’s situation is different. After all, I’ve been driving for 48 years now! That’s almost half a century behind the wheel, mostly accident-free and ticket-free. Typically, as you get older, you become 'low risk' for insurers, which is a nice perk.

Let’s break down the two main components of auto insurance:

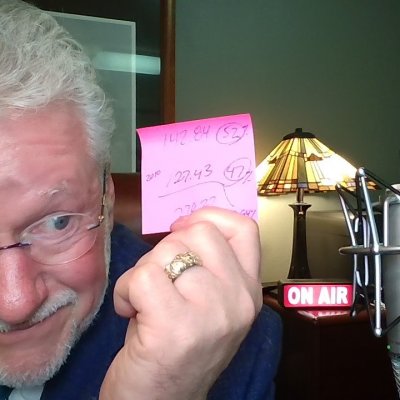

Liability Coverage: This often surprises people because they tend to focus on getting their car's value back after an accident. But liability coverage is crucial—it’s about protecting yourself if someone sues you or if you need to sue someone else. For me, 53% of my premium goes toward this. It covers injuries and underinsured/uninsured drivers.

Replacement Cost Coverage: The remaining 47% of my premium covers the actual value of my car. After some online research, I found that this portion of my premium equals about 3.64% of my car’s total perceived value.

Why bring this up? Because it’s all about trade-offs—whether it’s auto, homeowners, or “what if” insurance. You might go your whole life without an accident, without a deer smashing into your hood, without hail damage, and without anyone backing into you.

Now, let’s talk about another crucial type of “what if” insurance: disability insurance. Imagine you’re 35, earning $50,000 a year, and you need coverage until age 65. You’d need $1.5 million in disability coverage. Most employer-paid disability plans might replace 60% of your income, and that’s usually taxable. Plus, if you start receiving Social Security benefits, your employer plan is often reduced by whatever Social Security is giving you. So, you're stuck at 60% of your pre-disability income—not the full amount.

Consider this: if you die, your family won't receive that $1.5 million worth of income you would have brought in. It’s the same trade-off principle. Your auto insurance replaces your car, and life/disability insurance replaces you. You are your most valuable asset.

If we apply the same 43%/57% premium percentages to the $1.5 million in disability coverage for a 35-year-old until age 65, multiplying $1.5 million by 3.64% gives a premium of $54,600! Thankfully, the actual cost of proper disability or life insurance coverage is much, much lower.

So, if you’re willing to spend 3.64% of your car's value in premiums to insure its replacement, why not invest in insuring your human life value? It’s all about making smart trade-offs.